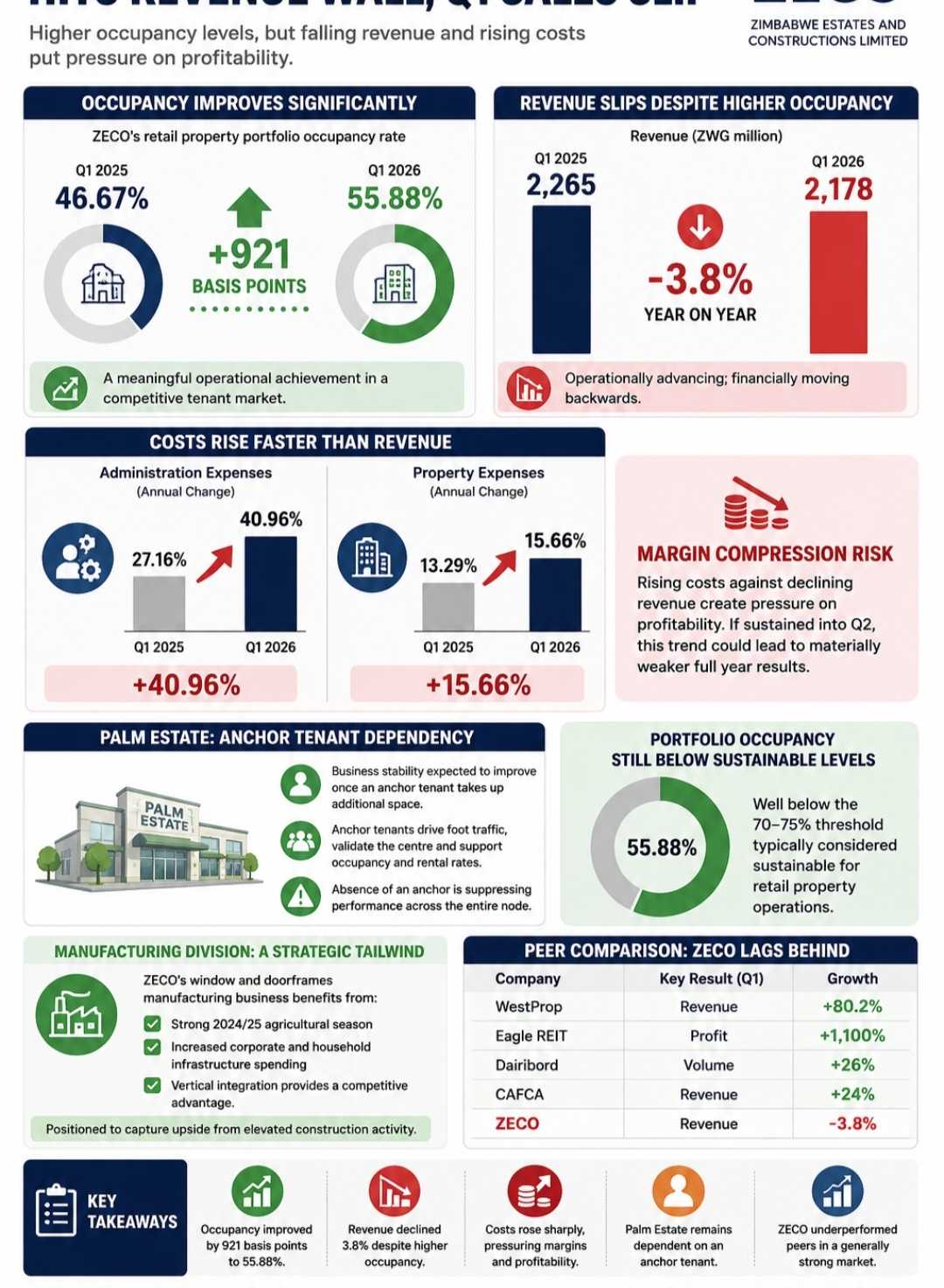

ZECO’s retail property portfolio recorded an improvement in occupancy levels during the first quarter ended 31 March 2026, but the gains were not enough to prevent a decline in revenue, highlighting a disconnect between leasing momentum and income performance.

The company’s occupancy rate rose to 55.88 percent from 46.67 percent in the same period last year, representing a 921 basis-point increase. The improvement reflects stronger leasing activity in a competitive commercial property market where landlords continue to compete for a limited tenant base.

However, despite the higher occupancy, revenue declined to ZWG 2.178 million from ZWG 2.265 million in the prior comparable period. The drop suggests that improved space utilisation has not yet translated into higher earnings.

ZECO attributed the weaker revenue performance to broader macroeconomic conditions, including tight monetary policy and currency stability, which have affected pricing dynamics and overall tenant spending capacity.

At the same time, operating costs increased sharply. Administration expenses rose by 40.96 percent, accelerating from the previous year’s 27.16 percent growth, while property expenses increased by 15.66 percent, up from 13.29 percent. The rising cost base against declining revenue points to growing margin pressure for the group.

Related Stories

Although the company did not disclose full profit figures, the trend suggests potential earnings strain if current conditions persist into the second quarter.

A key concern remains Palm Estate, where ZECO says performance is expected to stabilise once an anchor tenant takes up additional space. The reliance on a single tenant event underscores a structural vulnerability, as anchor tenants typically drive foot traffic, support surrounding occupancy, and underpin rental stability across retail developments.

Despite the occupancy improvement, ZECO’s overall portfolio level of 55.88 percent remains below the 70 to 75 percent range generally considered sustainable for retail property operations, suggesting that parts of the portfolio are still underperforming.

The company’s window and doorframe manufacturing division continues to provide some diversification support, benefiting from increased construction activity linked to strong agricultural output and broader infrastructure spending. However, the trading update did not provide a breakdown of the division’s contribution to group revenue.

ZECO’s performance also contrasts sharply with peers in the property and consumer sectors, many of which reported stronger growth during the same reporting period. WestProp posted robust revenue expansion, Eagle REIT recorded a significant profit surge driven by high occupancy at its Mazowe Walk Mall, while other listed firms such as Dairibord and CAFCA also reported solid growth.

In contrast, ZECO’s revenue decline suggests company-specific constraints rather than broader sector weakness, driven by relatively low occupancy levels, rising costs, and dependence on delayed tenant commitments at key assets such as Palm Estate.

Leave Comments